How To Earn $100k Passive Income For Life From A $200k Investment In 10 Years

SAFEHOUSE Algorithm Revealed: A $200k Investment In Indiana Real Estate Grows To $1.6 Million In 10 Years, Giving You $100k Passive Income Forever While Your Equity Continues To Grow

And It’s 100% Passive - Everything Is “Done-For-You”

Here is how it works:

1. Invest $200k and buy $800k worth of single family rental homes in Indiana using the Safehouse Algorithm. (which I will teach you shortly)

2. Reinvest all the income from these properties to pay down the mortgage for approximately 10 years. This is our GRS Strategy (Get Rich Slow).

3. In the 11th year of your investment, when your houses are paid off, you can start pulling out $100k per year to live on and spend as you choose. This is our $100k Launchpad.

4. Your properties by then are worth $1.6 million (based on 30 year historical appreciation in the areas that fit our algorithm). We call this The Millionaire Outcome.

5. Your property values continue to rise by $160k every year, while at the same time, you earn $100k annually to put in your pocket. This is the Lightspeed Growth Accelerator. It keeps growing while you sleep.

6. AND… the $100k per year INCOME you pull out also increases by about 5% per year (forever). This means your income adjusts upward with inflation each year, giving you more income every year. A perfect hedge against inflation. We call this, the Generational Wealth Outcome.

I know it sounds like a lot of work, right? And you’re right, it is. It’s a massive amount of work to plant, nurture and harvest.

But you don’t have to do any of it, my team and I will do ALL the work for you.

WE DO EVERYTHING.

Even though this program is fairly new, this isn’t something we just started. We’ve been creating millionaires for decades. We’ve built so many million dollar portfolios over the years, we’ve lost count.

We’ve done it many times, for many families… and we can do it for you.

I grew up in the 60s and 70s spending part of my summers as a kid on an Indiana dairy farm with my Aunt, Uncle and cousins – a tiny little farming town called Redkey. We had so much fun together, but while we played, I also learned a lot about husbandry, agriculture, and patience.

I learned the three phases of growing things.

- Plant

- Nurture (water)

- Harvest (eat)

If you screw one of these up, you don’t eat.

It’s the same with business and investing. If you want to grow your assets, if you want to create passive income and generational wealth, you have to build it with care. You have to be systematized, deliberate and consistent. You can’t drop the ball.

But we know that’s hard to do if you have a busy life. Most people just don’t want to think about it and they push it out of their mind.

That is why we created and use the Safehouse Algorithm. It allows us to do the planting and nurturing for you. It makes it possible for you to completely ignore your investments and know that they are being cared for and watered and growing. And it allows you to know that when it’s time to think about those investments again, they will be there, ready and IN FULL BLOOM – waiting to be harvested. Here is…

The Safehouse Algorithm

1. Planting [We’re going to leverage some of your available capital and put it to work.]

2. Nurture [The GRS Strategy (Get Rich Slow) IF YOU WAIT, YOU WILL WIN]

3. Harvest [The $100k Launchpad] This is when you get to spend the money.

4. Compound [The Millionaire Outcome] This happens automatically when you activate the algorithm.

5. Passive Income (Equity x Production) We call this [The Lightspeed Growth Accelerator]

6. Forever Fund [The Forever Fund Generational Wealth Outcome]

Once we build generational wealth for you and your family, it’s up to you to take the final step in the algorithm and…

7. Pay It Forward and help others do the same. This is what we did on the farm after the harvest, we’d share the wealth. There was enough for the whole community.

This whole Safehouse Algorithm is about strategy, growth, and outcome.

Now I’m going to show you multiple scenarios for building a million dollar portfolio in 1 year, buying only 5 houses.

$100,000/Year PASSIVE Income

It will also set you up to make $100k a year in passive income for the rest of your life… and your kids lives’ too.

I’ll show you how to easily scale and double, triple, and quadruple it year after year.

Over the years, I’ve had so many of my students accomplish and exceed this goal. Here are a few (160+) case study interviews with my students:

If you want to build long-term, reliable, consistent, PASSIVE income, I think you’re going to find the rest of this webpage very exciting.

It is about building passive income with investment capital, but I can also show you how to do it without capital and without credit. I know that not everybody has money to invest.

I teach zero down, no credit techniques in my Six Month Personal Mentor Program. For details, go to: www.ZeroDownInvesting.com

BUT…

You may not want to take the time to learn how to be a real estate investor and do the work necessary to build a business. You may not HAVE the time if you are busy making a living at a high paying job you love. I love being a real estate investor full time, but it’s not for everyone.

SO…

If you HAVE money and credit to invest, you don’t have to do it yourself. I’m going to show you how to leverage your money for the highest possible return and the least amount of risk. We can create a cash machine that will feed you for the rest of your life.

In fact, if you have some money to invest, my team and I will do it for you. You won’t have to do a thing.

There are three goals for EVERY deal you do.

1. Cash now

2. Cash monthly

3. Long term equity

You want to buy ‘Forever Houses.’ My friend Azam calls them “Safe Houses.” I love that term because owning these properties gives you safety from every storm. They give you income, security, reliability, and growth.

These are houses that will pay off over time and feed you and your loved ones until you die. And after you die, they become generational wealth that will continue to earn money for your kids until they pass it on to their kids.

I don’t know about you, but being able to give my kids a good life, a good education, the ability to follow their own heart and dreams – what better purpose can you have in this world?

And the best part, having this kind of passive income gives you TIME to live your life the way you choose instead of being tied to the millstone every day for a paycheck.

Time is the one thing you can never get more of…

Time to follow your dreams, time to spend with the ones you love, time to take a breath and just enjoy the fruits of your success.

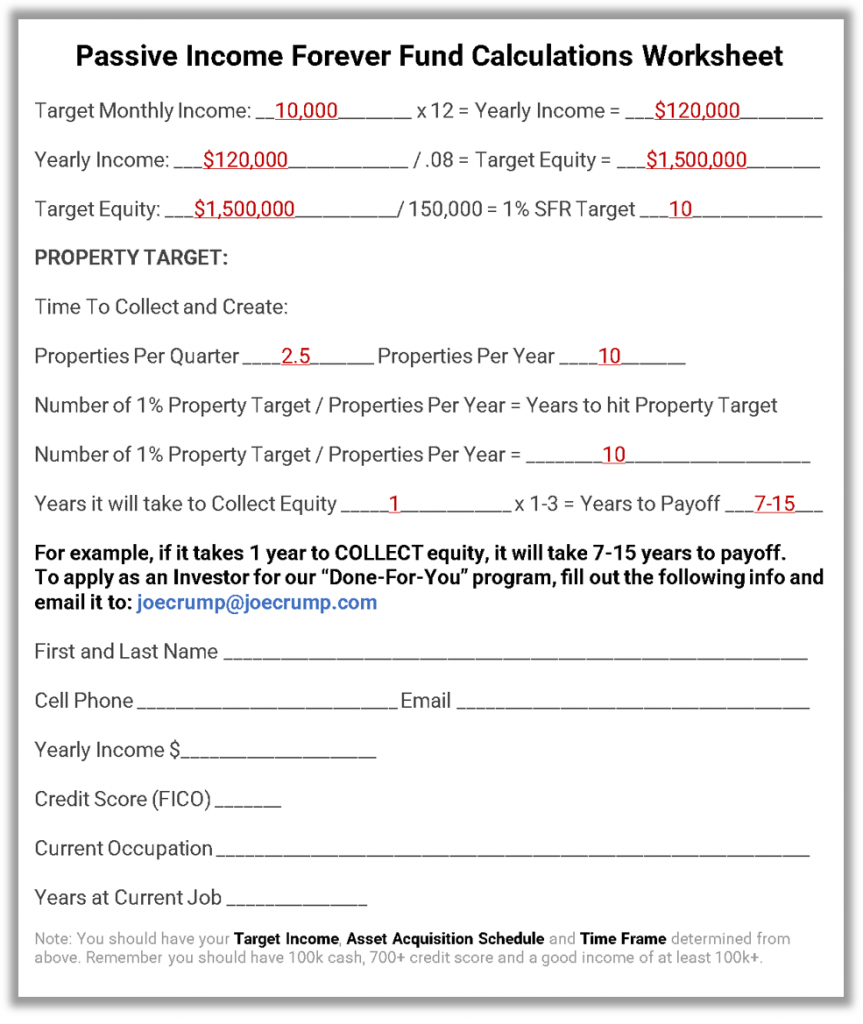

The Forever Fund Blueprint Calculator

($10k to $50k Per Month PASSIVE INCOME)

I’d like you to download this pdf worksheet: Forever Fund Worksheet Download – jr4.co/worksheet.

By the way, this worksheet was created by my friend and partner on this project, Azam Meo. I’ve known Azam since the 1990’s when at 17 years old, he came into my office looking to work with me and learn how to be a real estate investor.

He is my first multi-millionaire success story and my most successful student. I’m really proud of what he has accomplished and the man he has become.

Since then, he has far surpassed what I taught him and gone on to build an incredible business that not only has made him and his team millions of dollars, he has also had a positive impact on the world, working with special needs kids and so many other worthy causes. I’m sure he’ll tell you more about it if you work with us. I’m so excited to be working with him again.

I want more Azam’s in my life. I want more Daniel’s, and Bill’s and Pam’s and Shelly’s, Ron’s and Nina’s. These successful entrepreneurs, these HEROES, are my students and they are the people who make my job so much fun.

You know… people always ask me about other real estate “gurus” and all those other real estate facebook, youtube and instagram people out there. I tell them, the SINGLE BEST way to evaluate anybody in this industry isn’t by their deals, their cars, the big house they’re standing in front of…

It’s ALWAYS about the quality of their testimonials. It’s about the OUTCOMES. Specifically – when those success stories are about people who started with ZERO and created a REGULAR predictable, reliable, safe income. Those are the stories you should listen to. That’s the proof in the pudding.

So…

Let's Do The FOREVER FUND Math:

How Much Do You Want To Make?

$10k, $20k, $30k, $40k, $50k Per Month?

Forever Fund Worksheet Download.

Let’s plug in the numbers…

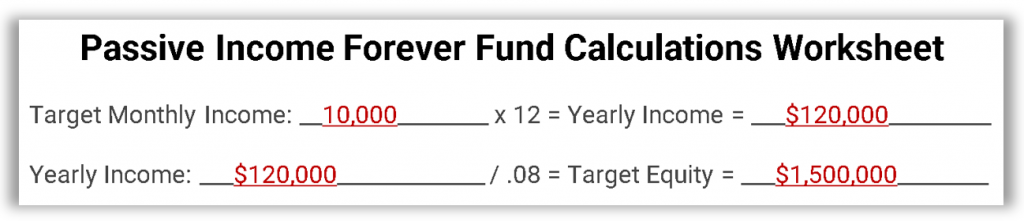

Let’s say you want to insure $10,000 of passive income every month for the rest of your life.

Plug in $10k.

The worksheet does the math and multiplies it by 12 months – so you have $120k annual income.

Next divide that $120k annual income by .08 – or 8%. That will tell you how much equity you need in order to earn $10,000 a month.

$120k divided by .08 = $1,500,000

That’s the amount of equity you need to produce $10k per month at 8% production.

You can use this formula for ANY amount you want to make. If you want to make $50k per month, just multiply $50k by 12 and you’ll get $600k annual income. Then divide that by .08 and you will discover your target equity needed to make that income – $7.5 million in equity. So if you want $50k a month, you need $7.5 million in equity, making you 8%.

Let me show you why we’re using .08 in this equation.

It's All Based On What We Call “1% Homes”

These are homes that bring in a net income of 1% PER MONTH of the total value of the property. So, on a $120k house, 1% is $1200 per month.

We look for houses that are making approximately 1% of their value per month. Most homes in the $100,000 to $175,000 range are able to make 1% monthly.

If we go over $175k or $200k, most single family residences (SFRs) in those price ranges make LESS than 1%. You CAN buy duplexes that will bring in 1% at those prices – we do those too, by the way, but there are fewer of them available. We want easy, plentiful and scalable instead.

You can also buy houses that make more than 1%. For example, you could buy a house for $40k that makes $800 a month income – that would be a 2% house. Or a $20k house that makes $600 a month – that would be a 3% house.

Cheaper houses have the potential of making you more monthly income, but you have to deal with more transactions, more tenants, bigger problems, more maintenance issues and worse economic areas. So if you want a more hands off approach, you should consider buying houses that are a bit higher in price even if they have a lower return.

Buying 1% houses is the sweet spot, the Goldilocks Position – not too expensive, not too cheap – JUST RIGHT. So that is what we go after for the portfolios we build. There are exceptions to the rule, but let’s stick with this for now.

That means we need to look at homes in the $100k to $175k price range to see this kind of consistent, reliable, easy to create return.

There are lots of ways to buy houses and make money, but some ways are easier than others. The path I’m taking you down is the easiest way to build a million dollar portfolio that makes you 6 figure annual passive cash returns. Especially since we are doing everything for you.

WE LOVE 1% HOMES

1% a month x 12 months = 12% income a year

Banks will typically allow you to apply 70-80% of your income toward the debt service (your loan payment) on a loan. The reason they do this is to make sure you have enough income to pay your taxes, insurance, property management, repairs and vacancy.

So the banks allow 70-80% of the gross income. – that works out to 8.4% to 9.6% return. (12 divided by 9.6 = 80%)

We figure if the bank will allow 8.4% to 9.6% return (and we know how conservative they are), we should be even more conservative in our thinking and base our model on 8%. (12 divided by 8 = 66.6%) So we are basing our monthly income figures on 67% of the property’s income. Very conservative, very safe. It would make a banker happy.

8% Is A Safe And Conservative Return

If you have a 1% property, you should be able to produce at least 67% of that property’s income.

So that’s how we came up with the 8% we are using in our calculation of how much equity you need in order to create a particular amount of income.

REMEMBER THE EQUATION PADAWAN

Equity x Production = Passive Income

If you want to make $10,000 a month passive income, you will need…

1,500,000 (Equity) x .08 (Production) = 120,000 (Passive Income)

If you want to make $50,000 a month in passive income, you will need…

7,500,000 (Equity) x .08 (Production) = 600,000 (Passive Income)

You can scale your income to any monthly income you like by understanding this simple formula.

We’ll come back to the worksheet later, but let’s take a look at an example property to help you better understand how to make this all work for you.

Example Property

Here is an example property:

There are quite a few of these properties available with these numbers in Indiana right now if you know how to find them.

If we built your portfolio for you...

We would purchase a house like this and get it rent ready for approximately $150,000.

And it won’t be exactly $150,000. The houses we find for you will be anywhere from $100,000 and $175,000 based upon the income, value, rents, etc.

We’ll pay full market value, by the way. This is the same method the big hedge funds are using.

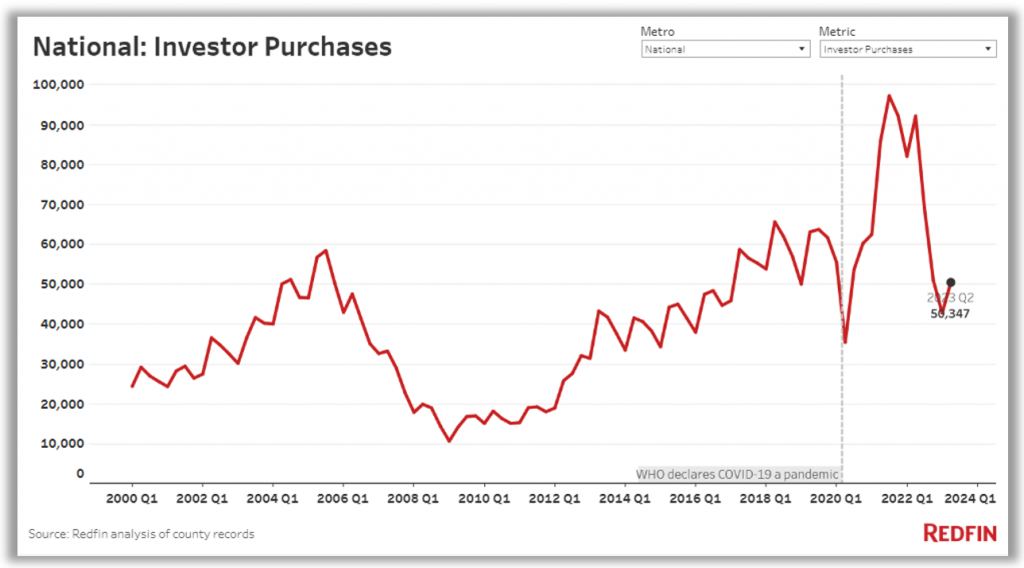

Twenty percent of all single family homes sold in the United States over the past 5 years have been purchased for full market value by big and small investors… mostly big.

There's A REASON The Big Money Is Betting On Single Family Resident (SFR) Investments

Here is how it works…

You will probably put down 20%, depending on the type of loan you qualify for and what the best scenario is at that time. Loan programs and rates change frequently. You will also come up with about 5%-7% for closing costs, points, appraisal, etc.

So, let’s look at the numbers with 20% down.

Based on a hypothetical $150k purchase price:

20% down is $30,000. So that means a $120k loan – 30 year 9.5% – PI $1001

If closing costs are 5% of the loan amount ($6000) – your total investment in the deal – $36,000

You Will Buy 3 to 10 Homes Depending On The Capital You Want To Invest

If you are investing $120k to $400k that means you can buy 3 to 10 homes at this price:

With 20% down and $120k investment:

$120k divided by $40,000 = 3 houses

With 20% down and $400k investment:

$400k divided by $40,000 = 10 houses

I’ll show you some real world numbers on a property we just purchased for one of our Hero investors in a bit. But let’s start with a hypothetical deal.

The example $150,000 properties I’m showing you here will rent for about $1500 per month.

IMPORTANT NOTE:

Once you close on the purchase, we will raise the price and rent it on a lease with an option to buy. The costs to sell on a lease option is covered by the buyer. The seller (you) receive the other half of the lease option fee as payments over the lease option period. More on this later.

“Origination and Acquisition” costs are collected at closing and total approximately: (Origination $1600 + Acquisition $2123 + Administrative $290 + Legal $984.23 = $4997.23 total). We attempt to negotiate these costs into the purchase price as seller paid costs.

So…

With a 20% down deal, your monthly cost is approximately:

$1001 P&I

$200 T&I

Total $1,201 PITI

You also have property management costs (if you want them to be managed – you do) at 10% of the income, so $150 a month.

So your cash flow is as follows:

$1500 gross monthly income

minus $1,201 PITI

minus $150 management

Total $149 positive cash flow

If you apply the $149 a month toward your principal loan amount, it will pay off in about 12 years rather than 30. That means you will have regular passive income from your portfolio in nearly ONE THIRD the time.

I can’t stress enough how much you save by putting this extra bit of money toward principal each month. Money that you don’t have to do ANYTHING to come up with – it’s income to you that is built into the deal.

YOU SAVE 18 years of $1001 a month (P&I) payments that you DON’T have to make. That totals up to a savings of $216,216 per property. Money that goes DIRECTLY to you – to your bank account. Money you can spend or reinvest.

More Streams Of Income From These Investments

There are ALSO other streams of income with an investment like this. This is the gift that keeps on giving.

1. Tax Depreciation. You will make about $1,000 a year in actual tax deferral from the IRS on each of these houses through depreciation. That is cash-in-your-pocket savings that you don’t have to pay until you sell the property. This is another reason to never sell. Talk to your CPA for details.

2. Buy-down on the note. Each month, part of your payment applies toward the principal. As I explained earlier, the more you pay monthly, the faster you pay off the loan. But the goal is to let the tenants pay for your house. We set it up for you and put it on autopilot, so you don’t have to worry about it. Set it and forget it.

3. Appreciation. I can’t guarantee the property will rise in value and there is the small possibility the lease option buyer will exercise their option, but historically, over the past 30 years, appreciation on these types of properties has been 10% per year. So about $15,000 per year. Every 10 years for the past 30 years, houses have increased in value by 100% – so 300% over the past 30 years.

Now multiply those numbers by 3, 5 or 10 properties over the next 5, 10 or 15 years and it starts becoming very attractive.

One more huge benefit…

Lease Option Buyers Are The BEST

We are going to sell your rental property as a Lease with Option to Buy – a ‘Rent to Own’

The biggest advantages to selling Rent To Own are:

- It means your buyer is paying to help you find and fill your house and not you. What they pay reduces your costs to invest. And we do the work for you.

- And my favorite advantage of lease option buyers is – Our proprietary Lease Option contract puts the responsibility of caring for the house on the Buyer’s shoulders.

We tell them, “When you buy a house like this, we want you to treat us like Bank of America. If your toilet stops up or your window breaks, do you call Bank of America? No, you take care of it yourself. It’s your house. You are responsible for it.”

You Don’t Wash A Rental Car

Nobody washes a rental car. You wash your OWN car. We change their mindset from being a tenant to being an OWNER. When you put a tenant in the role of a buyer, they are more likely to take care of your property. Also, most LO buyers don’t exercise their option. We’ve found it to be substantially less than 30%. You win either way, but if they don’t exercise the option, you win bigger.

So that’s a pretty rosy picture of it all.

And I’m pretty confident in what we are doing. After all, my students and I have implemented this strategy many times over the past 30 years. It’s how I built my own portfolio. It’s how all my successful clients and students have built theirs.

So…

What Could Possibly Go Wrong?

Well… A LOT, actually.

Every investment has risk and it’s possible, even with the best investments, to lose ALL your money.

Let’s look at a few of the hazards of buying houses like this.

Negative cash flow. Your taxes could go up and your rents could go down. You could have a vacancy. A tenant may damage your house and you’ll need to pay to get it repaired. You may need to pay an attorney to evict a non-paying tenant (this is usually taken care of by the property manager).

It’s important to know your risks and be prepared for them. If you don’t have any reserve funds, this may not be the right investment for you. I suggest you ALWAYS keep a reserve for emergencies. When my reserves get low – and sometimes they do – I make sure to get them back up as quickly as I can.

My experience as a landlord has been mostly good. All my properties are professionally managed for me, so when there is a problem with a tenant or work that needs to be done, I’m NEVER the one who gets a phone call from that tenant in the middle of the night. In fact, they don’t even know who I am. They talk to the property manager who solves the problem without me.

I’ve owned properties for 35+ years. I’ve seen it all. I’ve had properties damaged. I’ve had tenants who couldn’t or wouldn’t pay. I’ve had to pay attorneys to evict non-paying tenants. I’ve had storm damage that needed repair. I’ve had clean-up work that needed to be done after the last tenant. All of this is handled by my property managers. I don’t do any of that work.

I haven’t been to see many of my properties in over a decade. Some I’ve never seen. I just read the QuickBooks reports my bookkeeper and property manager create for me every quarter.

Sometimes, the manager must ask me for money to pay for damages or expenses and I’ve sent it to them. But when you have a portfolio, it gets easier. I have quite a few properties, and I’ve never had a situation where all of them had problems at the same time – knock on wood. Most of the time, the costs of the problems are covered by the income from the other properties I own. So I don’t need my bookkeeper to send the property manager money very often.

The worst time for me as a landlord was in 2008. We usually have a 3% vacancy rate in my portfolio – which is normal and pretty easy to manage. But in 2008, when the crash hit, my vacancy rate jumped up to 20%. It took about 6 months to get everything stabilized.

Values Dropped Almost 30%

But my rents didn’t go down.

Even though my property values dropped, I wasn’t very concerned because I was NOT going to sell them and I knew the values would come back up eventually. They did, within just a few years and have now vastly exceeded what they were before the crash.

My Rents Have Increased - My Property Values Have Increased AND My Mortgages Have Paid Off

The reason none of this was a disaster for me was because I had reserves in the bank to cover my mortgages and other expenses during emergencies. You don’t need a lot, but it’s very helpful to have some.

Overall, problems like this are just the cost of doing business. It happens to your stock portfolio too, you just don’t see the reasons why it’s fluctuating the same way you do when you own property. You also don’t have nearly as much control if you buy stocks. The stock market is a Blackbox compared to the relative transparency of owning houses.

"Your success is only limited by how much stress you can bear."

I’ve heard it said that “Your success is only limited by how much stress you can bear.” Every investment you make, every opportunity you grab, everything you do in life, entails risk.

I would argue that even sitting at home and hiding from the world, putting your money in a mattress, is risky. Life is risky.

My life has been dramatically better because of the measured, intelligent risks I’ve taken. Sometimes, problems happen and it sucks. I don’t always win, but mostly, life has been good to me and the ones I love because I was willing to take thoughtful, calculated, informed risks.

And… I doubt you’d be reading to this if you were mortally afraid of risk. You know it’s part of any profitable endeavor and any successful investment plan.

Azam said it best, “You have to be someone who doesn’t give a shit about that stuff. If you are buying properties like this, you can afford a new water heater or repairs or a new roof every couple decades because the bottom line is, if you WAIT, you will always win and because you have cash reserves, it gives you that cushion.”

That’s the beauty of long-term real estate investments. If you wait, you will win.

Ok, that’s the hypothetical stuff – the math of how all this works. What I want to do next is show you the investment breakdown of a REAL-WORLD DEAL we did for one of our Heroes.

We did this one just last week…

One House – Investment Breakdown

19.67% Return On Investment

$1,120 Per Month Cash Income – For Life

PLUS An Additional $1,400 Per Month (on average)

In Additional Revenue (see details below)

Last week, one of our Heroes bought this property. I’m going to breakdown how much it cost and how much he is likely to earn on it over the balance of his lifetime – and his kids lives – and their kids – on and on.

He is part of a very small group of people we are working with to build their own million dollar portfolios.

These are people who we handpicked – people that Azam Meo (my partner on this program) and I, personally approved.

These are people who came to us and asked us to build their portfolio. They are people who fit my criteria. Here are my criteria for who we approve:

- They have some cash to invest – a minimum of $120k – we may be raising that minimum soon.

- They have a FICO score that exceeds 700+. Basically, I want to work in this portfolio building program ONLY with accredited investors.

- They want to build a passive income stream of $100k per year that will feed them for the rest of their lives.

- We like them and think it would be fun to work with them.

- They understand that in real estate investing, IF YOU WAIT, YOU WILL WIN. This program is a long term strategy – we call it GRS – Get Rich Slow.

If you want to do it FAST, that’s possible too. You should get into my Six Month Personal Mentor Program. I’ll show you how to build wealth fast as an ACTIVE INVESTOR without using cash or credit. You can find out more at: www.ZeroDownInvesting.com

But in THAT program, you have to do stuff – ACTIVE INVESTING.

What I’m doing here, with this investor deal I’m about to show you, is a PASSIVE investing system.

You don’t do ANYTHING.

We do EVERYTHING for you.

We call our investors “Heroes,” by the way, because that is exactly what they are to us. We know what kind of guts it takes to step outside conventional wisdom. We know what it means to be entrepreneurial and take the road less travelled. We know what it means to aspire to more than ordinary. It takes a hero to do those things.

And, we find that most of our Heroes are also Heroes in their own lives. Quietly doing good in the world in whatever way they can. Quietly overcoming the odds to achieve the successes they’ve achieved in order to be a part of our program. That is one of the reasons we want to work with them. We are so proud of them.

So let me tell you about the property we bought for one of our “Heroes” this week.

I think the numbers are going to blow you away.

And remember, my team and I are doing ALL the work for him. He just has to come up with some cash and sign on the dotted line.

I’ve been teaching investors and helping investors build portfolios for more than 30 years.

Azam and I have made more millionaires in real estate over the past 20-30 years than anyone I know. And we can prove it.

I’ve had lots of students over the years make $100k+ per month and well beyond that. A couple hundred of them even allowed us to interview them about their successes. You can watch those videos here:

jr4.co/casestudy

But there is something I discovered...

There are two types of investors.

1. Those who make a pile of money regularly for a while and then go back to zero income when they stop doing the work.

AND…

2. Those who keep making money for the rest of their lives (even after they stop doing the work) and become part of the top 1%. Long term sustainable income that will never go away. Generational wealth.

The ones that accomplished #2 all have one thing in common – equity.

That’s the first secret to getting into the top 1% of income earners in the world and staying there – EQUITY.

The other secret is PRODUCTION, put those together and it creates PASSIVE INCOME. Long term, sustainable, passive income – generational wealth that allows you to “cross over” and enter the top 1% of income earners and never have to worry about regular income again.

Remember the secret formula I talked about earlier? Everyone should know this…

Passive Income = Equity x Production

The GRS (Get Rich Slow) is a way to do nothing and use the leverage of my time and my team, together, with your money, to create 4x your current equity.

It allows you to invest $200k and buy nearly $800k worth of property – in a few short months. (or $400k and buy $1.6 million)

It allows you to get more than 30% a year on your investment… forever.

Do you know of ANY other passive income stream that will generate those kinds of returns?

Of course not, because they don’t exist.

And PLEASE... listen to this next part very carefully...

Do you know of any investment that allows you to pull out money every month while the asset continues to grow?

With other passive investments like stocks, bonds, index funds, mutual funds, REITS, etc., when you pull out money from your account, your asset stops growing. If all you pull out is the income, the principal will stay stable, but it will stop growing. If you pull out your principal, your income will go down, your account will diminish in value and your return on investment will eventually drop to zero.

If you leave your money in stocks, bonds, REITS, whatever, they will grow over time. And that’s great. Just don’t expect it to keep growing when you want to pull out the income to live on.

THAT IS THE BIG DIFFERENCE WITH REAL ESTATE INVESTMENTS

The real estate portfolios we are building, you can pull out the income and your asset will continue to grow and appreciate over time. You can even refinance it and pull out the principal and it will still pay for itself and continue to grow… and if you do it that way, you won’t even have to pay taxes on the money you pull out!

You get INCOME and APPRECIATION at the same time.

What other investment will allow you to do that?

Okay, let’s talk about the property we bought for one of our “Heroes” this week. I told you I’d get around to it eventually.

We are in the process of building a multi-million dollar portfolio for him and, if all goes as planned, we should accomplish this within a year or less. Slow and steady wins the race.

So back to the house we are adding to our investor’s portfolio…

The property cost $155,000.

He is paying ALL cash for this house. He may eventually refinance the property and pull his cash out in order to leverage into 4 times as many properties, but for now, he has opted for the monthly income. His choice.

Most of our “Heroes” are leveraging their money so they can control more property. I’ll show you how that would work on this property in a minute.

But, on his deal, we negotiated our best price and we got the seller to pay $5,000 of the sellers costs to purchase the property, reducing his cash into the deal and increasing his return on investment.

This is a 1% house – just like we talked about earlier. It should earn 1% of it’s value every month in gross income.

In this case, it will rent for approximately $1,500 a month.

From That Income SUBTRACT...

Taxes – $180 month

Insurance – $50 month

Property Management – $150 month

Total Expenses – $380 per month

That Leaves A Positive Cash Flow Of $1120 per month X 12 months = $13,440 per year NOI

That is a 8.67% cash on cash return on his $155k cash investment.

Not a bad return, considering it’s not at all leveraged.

By the way, if you don’t leverage your investment, you won’t get as attractive a return, but it becomes EXTREMELY safe. Free and clear properties are just about the safest investment in the world.

But monthly cashflow isn't the only income this investment will receive.

You also get depreciation. I’ve explained depreciation in my other videos so I’ll just say here that it works out to about 1% additional cash return on the purchase price of the home. So if you are paying all cash, it’s giving you a 1% increase on your annual return on investment.

You will also get APPRECIATION on your investment.

As I mentioned before, over the past 30 years, property values have increased in Indianapolis by over 300% – more than 100% every ten years – and that’s EVEN FIGURING IN THE 2008 CRASH.

That means, historically, the value of your long term investment property doubles EVERY TEN YEARS. So…

(100% / 10 years = 10%)

This Adds 10% To Your Annual Net Return On Investment

That puts your annual return on an ALL CASH purchase at:

8.67% cash on cash return – rent income

1% IRS Tax depreciation

10% per year appreciation in value

That is a total of 19.67% RETURN

And this is if you pay ALL CASH.

If you leverage the deal and only put 20% down, you can buy 4 times as many properties and your returns almost triple. So let’s do that next.

Let’s look at the annual return on investment when you LEVERAGE and make payments on a mortgage.

Here is the formula for calculating the ROI (return on investment) on a LEVERAGED investment.

ROI = Net Profit / Total Investment x 100

A $155,000 house, here are the numbers…

TOTAL CASH INVESTMENT CALCULATED AS FOLLOWS:

$31,000 (20% down payment) + $8500 (closing costs – approx.) = $39,500 total cash investment

TOTAL NET PROFIT CALCULATED AS FOLLOWS:

$15,500 (10% annual appreciation) + 1500 (depreciation – approx.) + 1200 (annual buy down on the note) + $900 (rising annual rent) + $900 (positive cashflow after debt service) = $20,000

NOW LET’S SUBTRACT SOME POSSIBLE COSTS:

$540 (3% annual vacancy rate ($1500 rent x 3% x 12) + $900 (5% potential annual repairs needed – ($1500 x 5% x 12)

NET ANNUAL PROFIT:

$20,000 Net Annual Profit Before Possible Costs MINUS ($540 vacancy + $900 repairs) = $18,560 Net Annual Profit

$18,560 Net Annual Profit / $39,500 Total Investment x 100 = 46.99%

RETURN ON INVESTMENT

46.99%

So that’s insane, right?

Maybe we’re being too generous with the appreciation. Properties have appreciated 10% (on average) EVERY YEAR for the last 30 years, so it looks pretty solid. But let’s suppose it doesn’t appreciate AT ALL. That would reduce our Net Annual Profit to ($18,560 net annual profit – $15,500 appreciation = $3,060) That’s a lot less amazing.

$3,060 Net Annual Profit / $39,500 Total Investment x 100 = 7.75%

RETURN ON INVESTMENT

7.75%

The past 30 years tell us it’s going to appreciate. But if it doesn’t, for whatever terrible reason you want to imagine, you still have a decent return on your cash investment on this one property.

It’s not great compared to what we’re used to in real estate, but compared to stocks, bonds, mutual funds, REITS, virtually EVERY other type of passive investment out there – it’s competitive.

And if the worst DOESN’T happen, you get almost…

47% RETURN ON YOUR CASH INVESTMENT – IN ONE YEAR!

Why Are We Getting These Amazing Returns?

One word – Leverage.

That one thing.

Beautiful, real estate leverage. You sure can’t do this kind of massive leverage with stocks.

4X leverage

4X your equity

4X your buying power

4X your return on investment

4X your PROFITS!

When you only have to put 20% down to buy a property, you can buy 5 times as much property for the same money. Even if you figure in the cost of the money (closing costs), you can still buy 4 times as many properties. THUS – 4X LEVERAGE – you buy 4X the amount of property.

YOU GET INCOME & APPRECIATION

ON 4 TIMES AS MUCH PROPERTY

So in this case…

$155,000 (cost per house) X 4 (houses) = $620,000 (total value)

REMEMBER: The tenant is paying the mortgage FOR YOU. The property manager watches out for your asset. You pay off your loan and enjoy the appreciation and income.

So… with that said…

The big question you should be asking at this point is…

“How Fast Will The Tenant Pay Off My Loan So I Can Start Getting Monthly Income?”

If your mortgage is being paid by the tenant on a 30 year mortgage, how long will it take to pay off that mortgage.

A 30 year mortgage is going to take 30 years to pay off. Right?

If you have an 80% mortgage on a $155k property ($124k) at 9.5% interest, amortized over 30 years, your P&I (principal and interest) payment will be:

$1034 P&I

Taxes (on this property) – $180 month

Insurance – $50 month

Property Management – $150 month

Total Expenses – $1414.

That leaves you with $86 per month to apply toward principal.

If you don’t add any money to the payment from your pocket except that $86 each month, your 30 year mortgage will pay off in about 20 years. That’s a good start.

BUT, there’s no reason it should take 20 years, even if you don’t add a dime from your own pocket to the monthly payment. Let me show you why.

Your property manager will increase rents by 5% every year automatically (assuming you have a good property manager with ‘Safehouse’ policies). So, $1500 goes to $1575 in one year, $1625 the year after, $1700 the year after and so on. If you increase your monthly payment on the loan over time, just from the increase in rent – without taking ANYTHING out of your pocket – you will pay off your loan in about 12 years. You can do the math yourself, just google “appreciation calculator” and punch in 5% appreciation over 10 years. It jumps the rents from $1500 to $2693 per month over 12 years. That means when you pay off your loan, you will have a monthly NET income (after expenses) over $2,000+.

But we want you to own it even FASTER than 12 years…

(This power is built into our Safehouse Algorithm)

Here’s how:

We are going to sell your property to a lease option buyer to make you more money and pay off your loan faster.

Lease option buyers are the best. Remember how I said, they consider themselves OWNERS rather than RENTERS. We make them a ‘buyer’ because it makes them more likely to take better care of the property. It also makes them responsible for the repairs on the property – it’s all in our (rather brilliant) contract.

We will raise the price when we sell the house (so there is a profit to you above what you paid for it) and the lease option buyer will pay a non-refundable lease option fee. Half in cash, which goes to cover the costs of finding, qualifying and assisting the buyer – and half in payments from the buyer, which goes to you directly, so you can pay down your loan and build equity FASTER.

That should add an additional $200-$300 a month of income that will be paid monthly by the Buyer as “Down Payment Assistance.” This is paid in ADDITION to the rent.

If you add that $200 a month to your payment,

your 30 year loan will pay off in about 9 years

Are you starting to see how powerful an investment structured this way can be? This is our ‘SAFEHOUSE ALGORITHM.”

On top of the loan paying off, your property historically has nearly doubled in that period of time – so you will receive another $155k or so of equity (on top of the money used to pay off the loan) if appreciation continues the way it has over the past 30 years.

There are other ways to pay off your mortgages even faster. I’ll talk about those on a future video. But this guaranteed method is already built into our system using our FIVE proprietary “Safehouse Pillars” and you don’t have to do a thing to make it happen. We do it all for you.

So… our “Hero” (our investor) paid cash for this property because he wanted the income NOW.

Instead of doing all cash, he could buy 4 properties like this for the exact same investment and jump his return on investment from about 19.67% annually to 46.99% annually.

I know these numbers may be blowing your mind and hard to believe, but…

IT'S JUST MATH

There are no big leaps of logic here. Just straightforward calculations.

And if that’s true, why doesn’t everyone do it?

Here is the secret…

Just because you invest in houses doesn’t mean YOU are going to make this kind of money.

Most investors screw it up.

If you google the term “turn-key real estate investing” you’ll find real estate investors across the country trying to sell houses that they “help” you buy. Then they promise to get them rent ready, rent them out for you and manage them for you. There are even “under market value” wholesalers right here in Indiana doing it.

Some of these turn-key sellers are skilled investors with tons of experience and great portfolios of their own.

So what is the problem with them?

Well… that’s why I came up with this program.

They pretty much all SUCK.

I know that’s not a gentlemanly thing to say and I know it sounds harsh, but if you give me a second I can prove it.

And, honestly, I think you deserve to know.

Here’s the thing… I don’t need to do any of this. If Azam and I never work with another investor or do another deal, I hate to brag, but we’ll be fine, better than fine actually and MUCH better than I deserve.

I know I don't deserve this and I know how lucky I am and I'm SO grateful.

And because of the gift I’ve been given in my life, I know it comes with great responsibility to pass on that knowledge and that “luck” and make other people lucky.

That’s kind of the point of life, right? Whatever you were blessed enough to achieve (and I know some of you successful dudes think you did it by yourself, but you didn’t – our society, our parents, all the shoulders you stand on, made your success possible).

But because of that gift, you have a moral obligation to send the ladder back down for those behind you. That’s kind of the only way the world gets any better – people helping people.

If YOUR strategy is to build a society where you pull up the ladder behind you after you succeed so nobody can compete with you, well – then YOU kinda suck.

So we try not to do that. We try not to suck. I know most of you aspire to the same thing.

And one of the things I want you to understand is that doing what I suggest isn’t just about ANY house or rental property.

If that were the case, you wouldn’t need a “turn-key” investor and teacher like me to help you do it. You could just go out and buy any property and make millions.

Everybody would do it.

*deep breath*

All you have to do, is look at the math I just showed you to know that you should have started doing this stuff years ago.

WHY DID I WAIT SO LONG??

The best time to plant a tree is 10 years ago, the second-best time is today.

Stop beating yourself up and start investing today.

We help you build a portfolio and create passive income with Midwest real estate, specifically, right here in Indiana. Each house you buy makes you $1,000 a month or more, forever… eventually. The goal is to make at least $10k to $30k per month in 8 to 15 years when your mortgage is paid off.

Right now, the richest, most powerful people in world have determined that the single, most profitable asset class to invest in is single family homes, specifically, ones in the Midwest and definitely in Indiana.

Bezos, Musk, Gates, Blackrock they are obsessed with these homes and will pay almost anything to get them, because they know these properties are no brainers OVER TIME. It is what has been driving the real estate prices in this country. They play the long PASSIVE INCOME game well. It’s why 20% of all single family home sales in America over the past 4 years have been to investors and hedge funds like these.

Warren Buffet, who owns one of the biggest realty companies in the world, Berkshire Hathaway, knows that single family houses are good investments for billionaires like him, and he says, “Rule #1 for investors, DON’T LOSE MONEY. Rule #2, don’t forget Rule #1.” He knows that single family houses are a safe investment, or he wouldn’t be buying them. A safe investment in single family homes is a great investment that will make you money over time. IF YOU WAIT, YOU WILL WIN.

Our company is tiny compared to them, but we have a secret sauce formula for Safehouses with five criteria. I’m going to teach them to you in a minute. These five criteria, we call them “THE FIVE SAFEHOUSE PILLARS,” make it possible for us to compete with those titans and WIN – simply because we can do what they cannot. We are agile and robust and we’ve got boots on the ground. We can identify, build relationships with sellers and swoop-in and pick up the very best properties, enhance our investment efficiency and engineer the highest possible return on investment for everyone in our group.

That’s why we can buy the RIGHT houses – Safehouses – 1% houses – at or even ABOVE “market value” and still make 30-50% annually. We’ve made hundreds of videos on real life deals and have thousands of pages of real life success stories.

GRS – "Get Rich Slow."

Everything is designed to leverage your investment safely and then pay off that leverage as quickly as possible so you can get to that $1,000+ per month of “forever cash.”

This is one of our secret weapons to compete against the hedge funds and Wall Street guys. They can’t TOUCH our return on investment… just look at the REITs out there.

The first few years of a 30 year mortgage is the POISON period where most of your mortgage payment (90%+) is interest and goes RIGHT INTO THE LENDER’S POCKET. That’s why lenders will do anything to get you to refi in those first years.

That’s also why you want every bit of cash you can earn, thrown at the principal on that mortgage. That’s why we do lease option sales, so you can get that extra monthly income from the down payment assistance program we set up with the buyer.

We do lease options on yours and on our properties, so you can spend less time managing and more paying down the mortgage during that poison period. Our team follows our checklist. They know exactly what needs to be done and how to do it. I’ll give you the overview of the pillars of that checklist next.

When our team fills a property, they usually take the full down payment as their fee, but with this program, with our portfolio buyers, our “Heroes,” we negotiated a better deal for you and it only costs HALF of that. We cut them because we want the other half to go to you in the form of monthly payments from the buyer over the next 3 years – usually $200-$300 per month.

This will allow you to apply those funds to the principal on your mortgages.

Genius, right? We thought so – *shrugs modestly*

The best way to succeed is by working with someone who understands…

THE FIVE SAFEHOUSE PILLARS

SAFEHOUSES ARE what we call the houses you buy for long term generational wealth. The houses you buy to create a financial safe haven for yourself and your loved ones, now and for generations to come. 1% houses.

When we work with our “Heroes” and create for them a multi-million dollar foundation of homes that eventually pay off and provide for them monthly income of $10k, $30k, $50k or more… every month, forever – we almost always hear the same thing from them.

They tell us:

“There is nothing like the feeling of safety these houses bring to us. Knowing that income will be there for me and my kids and their kids after them is like a giant weight lifted off my shoulders. I no longer have to worry about losing my job or becoming disabled or even dying. I know they will be cared for. I know they will live well.

I know that the money not only keeps coming in, it actually grows as a hedge against inflation as rents grow. And my kids can completely screw it up as long as they don’t sell… because it’s equity and production all rolled up into one, working for them while they sleep.”

We teach our Heroes to teach their children to NEVER SELL these houses.

Teach them the formula: Equity x Production = Passive Income

I once heard it said…

"Be the ancestor you wish you had."

Be the one who moves your family up the ladder. Be the one they remember.

Be the one, when those checks come into your heirs from your investments every month – from the investments you made today, they take a moment and remember you and silently thank you and bless you for your love, industry and foresight.

You are their EPIC ancestor.

Be the one they want to emulate.

Be the change you want to see in the world.

You need SAFEHOUSES – 1% properties that will PRODUCE the necessary PASSIVE INCOME on the target EQUITY.

When done correctly, a Safehouse will make you (and the generations that come after you) at least $1,000+ per month. By the time the loan pays off, $2,000+ per month… FOREVER.

So use our worksheet and do the math with how much “Forever Income” you want and KNOW for sure, it CAN be done – it’s just math.

If this is all true, why don’t you ever see success stories like this anywhere? I’ll cover that in a second… but first…

Let's talk about the SAFEHOUSE PILLARS...

SAFEHOUSE PILLAR #1 – The passive income formula (you need to know THIS BY HEART and like I said, put it on the fridge and teach it to your children):

Passive Income = Equity x Production

This simple MATH formula makes it possible to understand, in one sentence, how to make $5k a week or $10k or $20k. You have to know what you are trying to accomplish.

Otherwise, you are just “investing” without a goal. Know where you are going and the path will open up before you. That is why we ask you to fill out the worksheet. It shows you EXACTLY how many assets you need to achieve your monthly income goals.

As simple as it is, almost nobody gets this formula or the math and it’s why they don’t understand the second pillar:

SAFEHOUSE PILLAR #2 – Safehouse Financing – if you are going to leverage your money safely and efficiently, you have to get the right loan product that allows for the best combination of down payment, monthly payments, and rent to debt ratio for the best outcome. This can be complicated and requires a deep understanding of debt versus equity, of long term tax benefits, of asset protection and passive income protection, of retirement accounts – of everything you need to know to run a successful business.

You need to understand the relationship between profits and down payments, between points and interest rates, between closing costs and prepaids, between DSCR loans, Hard Money Loans, Private Money Loans, Banks, Credit Unions, and Finance Companies. It’s a massive amount of knowledge, but it’s all important.

If you screw up any of these things, it will cost you money, sometimes creating a catastrophic loss. Do you know anybody who has lost everything in real estate. I sure do. (read my story – lol)

If you don’t know these things, you better find someone who does, someone who knows them through experience, someone who has your best interest at heart. Someone who has your back. Someone who knows exactly what to look out for.

SAFEHOUSE PILLAR #3 – Safehouse Forever Tenants. Every investor is afraid of getting bad tenants.

YOU SHOULD BE AFRAID

If you don’t have good management, if your management team doesn’t have the right SOPs and policies, if they don’t adhere to ethical practices and fair housing, if they don’t treat their tenants with the respect they deserve, if they don’t have masterful bookkeeping – oh lord, I could talk about the importance of bookkeeping for hours and all the ways we’ve screwed it up over the years – don’t start from scratch – learn from our mistakes. Let our bookkeepers do it for you and send you the reports. Don’t do this yourself and screw this up.

Find management who have a deep reservoir of knowledge about how to find, care for and nurture tenants. Learn how to find tenants who will bring you the highest ROI. It’s a science and it can be taught, it CAN be systematized and policized – and it can be learned. Make sure your management team knows what they are doing.

The management company we are using here in Indiana, for this program, was trained by me many years ago. The owner came through my mentor program like nearly everyone who works or partners directly with me. Her name is Pam Madsen and she and her company manages my personal Indiana portfolio and she’s been doing it for nearly 25 years. When I frequently say that I haven’t been to see many of my houses for more than a decade, I can only say that because of Pam. I trust her like family and am deeply grateful for the work she does.

When I brought her into this program to serve my “Heroes,” our investors, she said to me, “Well Joe, I guess we’re not retiring anytime soon.” And we laughed together and then talked about how excited we were to be building millionaires again in this new program. We’ve done it before, so many times. We’re doing it again.

That brings us to…

SAFEHOUSE PILLAR #4 – Safehouse Forever Management – this is HUGE.

As a property manager, you will always repair a property differently if you are planning on keeping it forever than if you just want to keep a client happy “for now” (since they can dump you as the management). We don’t work that way.

When we fix a problem on a property, our goal is to fix it FOREVER, and yes, this sometimes takes more money, but over time, it “costs” you less.

Don’t be a slumlord – find property management who will take pride in your properties and make your communities better, not worse. People complain about too many rental properties in a neighborhood, but our goal is to have the nicest, best kept properties in the area. My question is always, “Would I live there?” If the answer is “Yes” I know we are doing something right.

SAFEHOUSE PILLAR #5 – This is the big one. This is the ONE Pillar that RULES THEM ALL.

SAFEHOUSE OUTCOMES

If you screw up even ONE of these pillars, the entire thing goes belly up, but if you don’t have this one, ANYONE can see, as plain as the nose on my face, that you don’t know what you are doing.

Remember, this process of building and holding real estate is a symphony. Even one drunk in the violin section ruins it all.

THAT is why you don’t see other companies like ours producing great results. They might be good at sales, or great at finding properties, or maybe they are nice people and you’d enjoy hanging out with them and having a beer. But they don’t understand these pillars and how important they are. Just ask them.

And because of that, they don’t have successful OUTCOMES for their investors.

They might have four or five or, maybe even ten or twenty ‘testimonials’ on their website (10 to 20 is very rare, by the way).

We have HUNDREDS of successful investors – our “HEROES.” And we interviewed many of them ON VIDEO and asked them to tell us the good, the bad and the ugly. We asked them what worked and what didn’t, what advice they would give to others who wanted to accomplish the same things.

We told them it’s okay to be critical – we know we make mistakes too. But one thing I think you’ll find by watching them – they are ALL excited – they have ALL had a life changing experience – you can see the excitement in their eyes and hear it in their voices. They make me so proud of them. You can read and watch some of these videos here: jr4.co/casestudy

I CHALLENGE you to find a page like this on ANY other “Turn-Key” company’s website – on ANY other teacher’s website. They just don’t exist.

THEY DON’T HAVE A TINY FRACTION OF THE

HAPPY CUSTOMERS AND CLIENTS WE HAVE

It’s all about OUTCOMES.

Remember earlier, when I said I can PROVE all the other ‘turn-key’ companies selling and managing properties suck?

THIS IS THE PROOF – THEY DONT HAVE ANY PROVEN OUTCOMES.

The OUTCOME is ALL that matters here.

With so many turn-key operations, so many wholesalers, bird dogs, investment gurus, realtors, youtube influencers – what do you NOT EVER see?

Outcomes. (period – mic drop)

Take a look at a few of our outcomes: Case Studies From Our Heroes

That’s what is missing in this industry and that’s why I’m doing this.

Many of these companies are just outright toxic and inept. I even know some of them who have gone to jail for mishandling their client’s money.

I can sit here and TELL YOU what they should do. I can teach THEM how to do it – some of them have been through my training. I can teach them why they should be ETHICAL, but I can’t make them act that way. I’ve been trying to do that since I started teaching real estate investing back in 1998.

LOOK AT THEIR OUTCOMES

If you find somebody who is using these 5 pillars effectively – PLEASE let me know – I’ll be their best client and student.

Work with the people who understand the five pillars.

1. The Safehouse Passive Income Formula – they can break down exactly what success is in ONE sentence. For example: ($1k+ passive income per month, per safehouse, FOREVER)

2. Safehouse Financing – how to pay off rentals at light speed, how, why, risks, benefits.

3. Safehouse Tenants – how to position your properties and your company for the best results and relations.

4. Safehouse Management – we have a construction company and FULLY fix things, do they?

5. Safehouse OUTCOMES – this is the most important, the key to know how to judge any company. Do they even have them?

Do you REALLY need to find someone who

implements ALL of these pillars?

No, just like you don’t need a parachute to go skydiving. You only need a parachute to skydive TWICE.

That is why other investment companies can’t produce proof of specific outcomes for their investor buyers. Too many of their people fall flat.

I’ll give you my full “Passive Safehouse Income Quiz” to test your knowledge in a minute, but for now, please make sure you ask yourself these three questions about ANY investment team, turn-key investor or wholesalers, or any other investment option you might look at:

a.) What is the definition of success in one sentence?

b.) Can I see their people achieving that exact definition of success?

c.) What is the exact criteria that makes their approach so different?

That last one is kind of funny, right?

If our approach is such a “secret” then why are we telling people? Well, that’s just it, we’ve been teaching this for decades and I know that almost nobody has the work ethic, dedication and CARE for their clients to put these five principles into practice.

How else can you explain our success stories compared to theirs?

HOW WE CAN WORK TOGETHER

So, you like the numbers, you like the strategy, you like the risk profile, you like the upside and understand the downside.

The only problem is that you would like someone who has done it before to be by your side.

Some of you just want someone to do it for you. You don’t want to spend months learning all the techniques I’ve learned over the past 35 years. You are busy at your other job. You are busy in your life.

You’ve got some money to invest and good credit. You know you need a better investment vehicle for your retirement, but you just don’t have the time to learn and implement a strategy like this.

If that’s you, WE CAN DO IT FOR YOU.

I’ll explain more in a minute.

The second type of investor is someone who wants to do it all themselves – or has to do it all themselves. Someone who may not have much money to invest. Someone who needs to use zero down and no credit strategies. Someone who needs income now and would eventually like to become a full-time investor. If that’s you, I can walk you through that process step-by-step as well, if you’ll let me.

You can find out more about my six month personal mentor program and the cost at:

If you have questions about the program that aren’t answered on that page, just send me an email to: joecrump@joecrump.com

***

IF YOU WANT IT ALL DONE FOR YOU...

My team and I are going to work with just 5 people to start.

For the first 5 people who fit my criteria, I’m going to build a portfolio for you.

I can only take on five people at a time because my team and I are going to do all the work and I’m unwilling to bite off more than we can chew.

WE DO EVERYTHING

We are going to build your portfolio. We are going to find the properties, set up the financing, get you to closing, get them rent ready, fill the properties with stable LO tenants and pass them to a competent property manager.

This is the ultimate “done for you” real estate investing program.

To qualify to work with us, you need 2 things.

1. At least $120,000 you can invest long term.

2. A FICO score above 700+

By the time we are done, we will invest your $120,000 to create your own cash flowing portfolio of 3 houses.

And if you have more money to invest, we can scale this and buy you as many as you want.

All you have to do is come up with the money and sign the paperwork. Our “IGYB Transaction Facilitator” will hold your hand and walk you through the simple steps.

We literally do everything else.

IGYB Transaction Facilitator

"I've Got Your Back"

When we are done, you will own a cash flowing real estate portfolio.

Then you sit back, collect the cash flow, and wait – typically 8 to 15 years. This is a BUY & HOLD strategy. During that time, the properties pay for themselves (actually, your tenants pay for them) and usually the houses go up in value (probably 50-100% over that period of time).

The properties will be professionally managed, so all you have to do is look at the bookkeeping reports you get monthly and watch the money come into your bank account.

To Qualify…

You need $120k you can invest long term and you must also have good credit (a FICO score above 700).

By the way… you don’t have to have that money in the bank.

If you have a cash value, whole life insurance policy, you can borrow the funds against it. Or, if you have a HELOC (Home Equity Line Of Credit) on your home, you can borrow against your house. I’ve done this personally with my house. I hate to leave all that equity sitting and doing nothing. You can also deduct from your taxes all the interest you pay on these investments.

If you have the funds to invest, we will help you find, rehab and manage a profitable, cash generating portfolio.

We will build you a portfolio of 3-10 investment properties right here in my hometown of Indiana. We will find them for you, fix them up as needed, fill them with paying tenants, and place them with professional management. You will keep them for as long as you want – forever, if you listen to me.

My philosophy, NEVER SELL. If you need cash, refinance instead.

If you need cash (for whatever reason) above the income the properties are generating, you can refinance instead of selling. You don’t have to pay capital gains on a “cash out” refinance and your tenants will make your payments. As soon as you sell, you lose a cash producing asset and you have to pay taxes on the gain.

Keep your properties!

We will set you up so you eventually have long term passive income of $1000 to $2000+ per property, per month.

Would an extra $6,000 to $60,000 a month improve your retirement? Would several million dollars in free and clear real estate, that is fully managed and maintained, BUT NOT BY YOU, give you more freedom and comfort when you retire?

This is the exact plan I used to build my own portfolio and I can tell you now, it has been very good to me. It feeds me every day and, if I don’t get stupid and sell, it will feed me for the rest of my life.

I also want to stress something that I think is VITALLY important

I’ve been in this business for more than 35 years and Azam has been doing it for 25 and…

I can't honestly think of ANYBODY in the world who has gotten more people $6k to $60k per month income and built more multimillion-dollar portfolios than we have.

We have more case studies and success stories than anyone. Check Them Out

I challenge you to find ANYONE who teaches real estate investing or sells TURN-KEY real estate portfolios like us, who has a bigger list of happy, successful students and clients.

GENERATIONAL WEALTH

Generational wealth comes from passive income reinvested. Our systems, training, and the work we do for investors, makes passive income available to EVERYONE.

You can ask us to do it for you or you can use our techniques to do it yourself and create assets in SET IT-AND-FORGET mode.

And once that’s done, time is your ALLY.

The difference is EQUITY

The reason so many people stay broke is because time is their enemy. We make time your friend.

And truthfully, there aren’t that many ways to build equity like this, let alone, better ways than this one.

You get paid based on what you DO, but you get rich from what you OWN.

We always talk to our clients and students (our Heroes) and we ask them why they feel so good about creating these income streams.

They ALL say some version of:

“For the first time in my life, I feel protected. I know that money will be there for me every month for the rest of my life. And then my kids, and their kids, will always have a base income that continues to grow over time and continues to feed them forever. It’s irreversible. There’s no feeling like it in the world.”

When I hear our HEROES say these things – with such deep gratitude and love, I know what I chose to do with my life made a difference.

****

If you decide to work with us, I’d ask you to fill out the worksheet I showed you earlier and send it to me. It will let me know if us working together is a good fit.

I can’t promise we’ll partner with everyone who applies. Sometimes it just doesn’t work, but I promise I’ll give you a fair shake, look at your situation, and tell you honestly whether or not we can help. And if not, I’ll give you suggestions on other paths you might follow that would better fit your situation. I’ll take the time to do this because you took the time to fill it out and send it in and I want to show how much I appreciate you doing that.

And – you might be a perfect fit to work with us, but if I already have my 5 investors, I’ll have to turn you down until another space opens up. So I want to be up front with you about all this.

OUR MISSION IS YOUR SUCCESS

Our mission is to make lifelong friends helping folks around the world create generational wealth with Indiana real estate and business building.

One of the best parts about my business is the relationships I get to build with the amazing entrepreneurial investors who work with us.

Only 3% of the world has an entrepreneurial mind set. Only 3% are willing to ignore the tired old advice of ‘investment experts’ they read in the news every day and break the paradigm and find a better way.

But I’m lucky.

100% of the people who come to us and work with us have an entrepreneurial mind set. 100% have the willingness TO BUY – TO HOLD and build a massive, multimillion dollar portfolio they know will give them passive income for life.

It’s a gift to be part of a business that draws these kinds of people to your door.

Well, that's it. You've got 3 options...

1. You can take this information and go out and implement this strategy yourself. I’ve got a book that might help you. www.JoeCrump.com/millionbook

2. You can get involved in my Six Month Mentor program and let me take your hand and personally walk you through the minefield. I’ll give you my step-by-step plan, my systems, my marketing, my contracts, my SOPs (Standard Operating Procedures), my proprietary methods for finding deals, talking to sellers, making offers and profiting from those deals. I’ll show you how to build your business from the ground up without cash and without credit – pulling yourself up by your own bootstraps.

It takes work, but it’s how I did it and so many of my students have done it this way too – out of necessity. Most people don’t have a pile of cash to invest when they are getting started and I understand that better than most because I’ve been there.

If you get involved, you will work directly with me, not some “coach” I hired for $25 a hour. Find out more about my mentor program here: www.ZeroDownInvesting.com

Or… finally…

3. You can let me build your portfolio for you. My team and I will do everything. This requires some money and good credit. If you fit that criteria, just download and fill out the worksheet, send it to me and we’ll get you going. worksheet Please don’t do this unless you are serious.

There’s one more option. This is the one that most people take.

You can do nothing.

Everything that is coming at you in life will keep coming at you, whether you prepare or not. There’s nothing you can do about that.

But what you CAN do is prepare yourself for it. Create a solid financial structure you can live comfortably on for the rest of your life and then pass on to the ones you love.

Life is so much better when you are ready for what comes.

That's all I've got for now.

If you want to work with me, fill out the worksheet and email me at joecrump@joecrump.com

Whatever you decide, I wish you all the best of all good things.

Joe Crump and Azam Meo

PS – We do other things too.

- If you would like to invest some cash into one of our projects and be a Private Money Investor, we have some excellent projects that will give you a secure investment and a great return on your money.

- We also make feature films for those of you who would like to be an “honest to goodness” real life movie Producer. If you would like to invest in our next movie, let us know. Making movies is my passion – it’s the hardest work I do and the most fun – and I invest my own money in these projects too. If you have the resources and are interested, we’re looking for partners.

- We also buy commercial properties. If you’d like to invest in commercial projects, let us know… especially if you are interested in RV and Boat Storage, Self-Storage and Semi-Truck Parking. These projects are safe, have enormous upsides, great cash flow and are in big demand.

- We also buy houses – lots of them. If you have one to sell or if you’d like to invest and buy some with us, just let me know.

- We also buy and invest in small and medium sized businesses. If you have a business you’d like to sell or need money to grow an existing business, let me know. We will consider anything.

Email me if you are interested in any of these opportunities. joecrump@joecrump.com

PPS – If you are interested in automating your real estate investing lead generation and putting your business and your team on autopilot, you should check out my investor software

www.PushButtonAutomarketer.com

It will allow you to generate low cost motivated seller leads every day for pennies. It will also allow you to do the most powerful drip marketing campaigns on the planet, including text messages, ringless voicemail, snail mail campaigns, email campaigns, and powerdialer campaigns for your call center or virtual assistant. This powerful CRM system can automate 90% of your real estate investing business. You can then outsource 9% so you only have to do 1% yourself. Extract yourself from your business today.

One Last Thing

PPPS – I know it’s hard to know who to trust in this business. When you are trying to decide who is real and who is ‘fly-by-night,’ look at OUTCOMES – who have they helped in the past and how well documented are those successes?

When you look at potential returns on your investment, look at the MATH – it doesn’t lie.

When you look for competence, look for a company who uses systems, policies, ethics and personal interactions.

When you look for experience, find the person who has been in business the longest with the fewest complaints and most kudos.

The time has come…

Are you ready for prime time?

The Passive “Safehouse” Income Quiz

TEST YOUR KNOWLEDGE

Test your knowledge of the Safehouse Pillars for passive investing by answering these questions.

(WARNING: The correct answers may induce gleeful insomnia.)

Do you think it makes sense to pay 20% down for the right kind of rental property?

A – Yes, as long as the cashflow works.

B – No.

If we have a lease option buyer ready to go who would give you enough money monthly to pay off your 30 year mortgage in 8 to 15 years (we love those deals), would that be a good fit for you? Why?

A – Yes

B – No

If each property we set up for you required a $40k cash investment to buy – AND in 10 years:

> the mortgage was paid off (free and clear),

> it was worth around $300,000 and

> it had a monthly NET income of approximately $1,500+ for the rest of your life.

Would a deal like that make sense to you?

A – Yes

B – No

We usually pick 1% houses that rent for $1500 and eventually produce a net of $1000+ to $2,000+ per month – forever, would that make sense for you?

A – Yes

B – No

C – It sounds too good to be true.

If these numbers work for you, would it matter to you how much money we make putting these deals together? Why?

A – Yes

B – No

What is the best way to find properties that fit the Safehouse Algorithm?

A – Find properties you want to live in.

B – Find someone who personally owns properties that fit the Safehouse Algorithm, understands gentrification and the benefits to investors, and who knows the areas intimately.

C – Find properties your Mom likes.

D – Find properties your Realtor and his dog would like.

What is the secret sauce for finding good tenants for your properties? Without this thing, your whole rental business collapses.

A – Zillow

B – A sign in the yard

C – A good property and an amazing, systematized management team with policies and standard operating procedures already in place.

D – There is no such thing as good tenants.

What policies, SOPs, systems and staff are vital for the success of your portfolio?

A – If the company you hire doesn’t have systems in place to run their company, don’t even consider working with them.

B – We don’t need no stinking systems.

C – Hire somebody who ‘goes with their gut.’

What amount of leverage is the ‘sweet spot’ for turn-key rental properties?

A – The amount of leverage that allows you to have enough positive cashflow to support the property AND use the income to pay off the mortgage in 8 to 15 years.

B – 5% down

C – 20% down

D – All cash

What do you need to know about the difference between loan products, leverage, interest rates, points and qualifications?

A – Nothing, just call any mortgage broker and let them worry about it.

B – Find a competent investor with a proven algorithm who understands the impact of all of these things on your purchase, hold and exit strategy.

C – Ask your personal trainer.

D – Consult your therapist.

When your management hires contractors to maintain your properties, what kind of work should you expect from them?

A – Put a patch on the problem as cheaply as possible.

B – Find a contractor on craigslist who is out of jail this week.

C – Find a company who uses approved, licensed contractors who fix problems so the fix will last forever… even if it costs a bit more.

D – Never fix problems to houses. Squeeze as much as you can out of them until they fall apart, then set fire to them.

How do you pull out $100k per year of passive income from a $200k cash investment after 10 years – without ever touching your equity?

A – Invest $120k in 1% Safehouses.

B – Buy Index Funds.

C – Invest in REITs.

D – Invest in Bonds.

E – Invest in Gold.

F – Invest in the Stock Market.

G – Invest in Crypto.

H – None of the above. This kind of return on passive investments doesn’t exist.

What is the single best way to KNOW if the “Turn-Key” company you are working with has positive OUTCOMES for their clients?

A – Does the main guy own a Maserati.

B – Do they have HUNDREDS of real life case studies and testimonials on their website that are on video and use their clients real names, faces and locations? Can the company PROVE their client’s outcomes?

C – Are there random pictures of happy people on their website standing in front of big houses.

D – There is no way to know if a company has positive outcomes. You just have to take a chance and pray.

Do you want to invest $120,000 and turn it into $900,000 of real estate equity in nine years, buying 1% houses that bring in $4,500 a month for the rest of your life? Your investment can be cash, an equity line, an IRA or 401k, a whole life policy, etc.

A – Yes

B – No

Do you have access to $360,000 to invest if you could turn it into $2.7 million of equity after 9 years and bring in $13,500 a month – forever?

A – Yes

B – No

Do you have $120,000 or more to invest in real estate?

A – Yes

B – No

C – I don’t have any money to invest. I’m interested in zero down strategies. Zero Down Strategies

Do you have a FICO score above 700+?

A – Yes

B – No

Did you fill out the worksheet and send it in?

A – Yes

B – No – Download Worksheet Here

C – I have some questions first: (email them to joecrump@joecrump.com)

Real World - Real People

Hello Joe,

Thank you so very much for all that you’ve done. You’ve been extremely nice and kind. That’s unheard of and none of the other guys would ever even consider doing the same. And to top it off, they never give you all the steps you need to complete a deal.